Portfolio update – November 2024

How to achieve financial freedom?It’s easy to say. It’s harder to achieve. For the future me is this journal entry. Starting from the year 2021, I describe the long way, point out the successes and the wrong decisions that I have made. I hope it will also motivate you to build your financial independence.

Summary

Exceptionally, instead of a month, this time after two I am writing a new portfolio update. Similar to last year, this year’s October/November is a vacation period for me, in which I use the extra days off. Hence the lack of time and even opportunity for a summary.

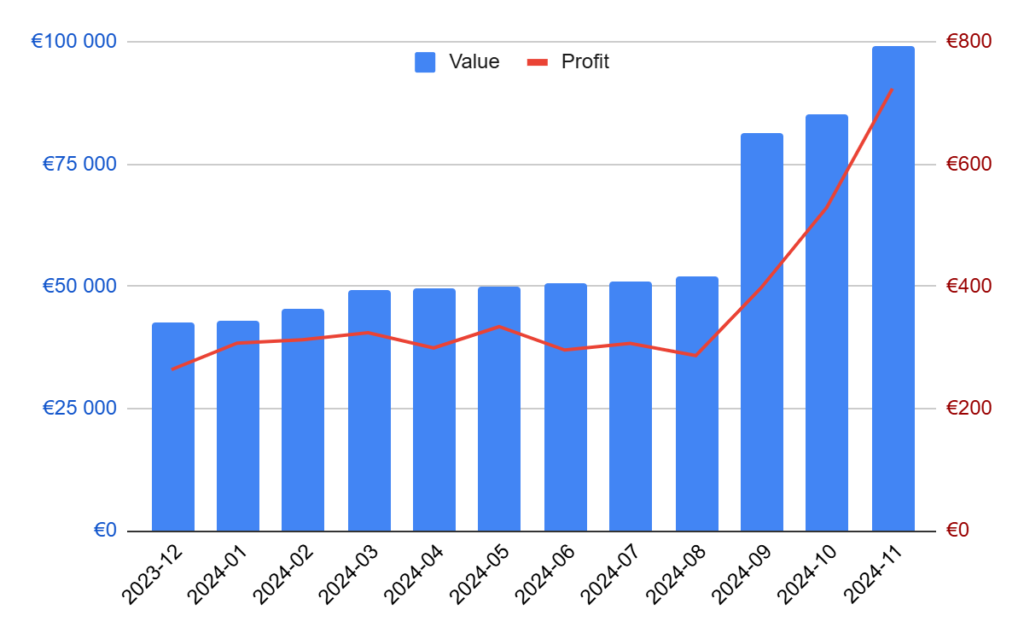

I continue my strategy of increasing my peer-to-peer portfolio. Over the last 2 months I have topped up over €11k. Reaching a portfolio value of €99k. It is worth noting that since August I have managed to practically double the entire value of my investment, and with it my income to over €800 per month.

As announced, I have added another platform to the basket, Debitum , which I have been testing since September. With such a large portfolio value, it is worth diversifying the risk across a larger number of providers. Debitum is a regulated platform and requires collateral for loans from its clients, which is an additional advantage. More arguments for and against in detail.

I invite you to a detailed analysis.

Portfolio history (last 12 months)

Portfolio summary

| Position | Value | Profit |

|---|---|---|

| Bitfinex Lending | €4 643 | €16 |

| Mintos (EUR) | €34 106 | €263 |

| Mintos (RUB) | €2 407 | €0 |

| Robocash | €20 435 | €176 |

| Esketit | €11 639 | €115 |

| PeerBerry | €15 118 | €78 |

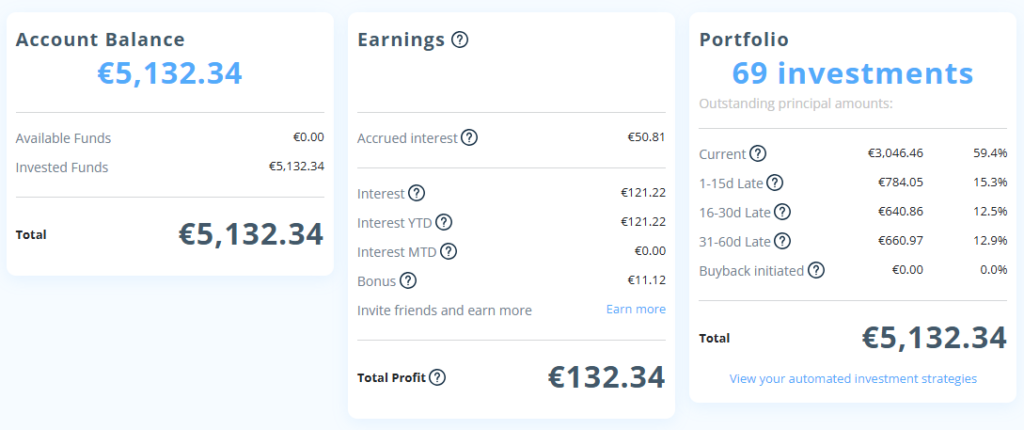

| Income | €5 132 | €55 |

| Debitum | €2 072 | €22 |

| ETF | €3 509 | €105** |

| Total | €99 060 | €726*** |

(***) Due to the lack of certainty of the exchange position, the ETF was excluded from the total profit.

Bitfinex Lending*

I remind you that 2 months ago I decided to withdraw almost 7k euros. This was due to the extremely low returns, even lower than the current savings deposits.

One is left with a smile seeing that a month after the majority of position were withdrawn, it started working sensibly (9.4% in October). Although the result is far from the returns of other platforms (10%+), at least something started to happen.

Graph of all loans sold in the last month:

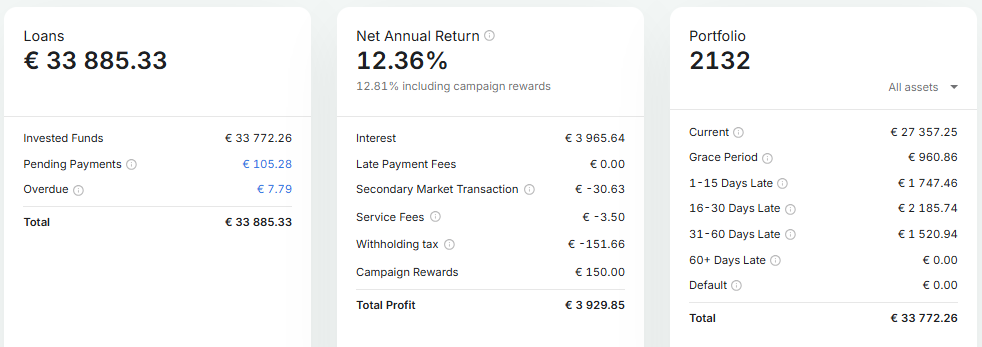

Mintos (Euro €)*

The first break through the barrier of 200€ of income per month is behind us. As the position is strategically the largest in the portfolio, and the position has grown over 30k euros, I expect to cross another barrier of 300€ of income per month soon .

There was a small change on the platform that made it impossible to count delayed loans according to my method . That is, from the list of delayed loans, add up the remaining part to be repaid (“outstanding principal”). Thanks to this mechanism, I always had a reliable picture of how many, after subtracting the repaid installments, I had “higher risk” investments. The system works independently of the platform.

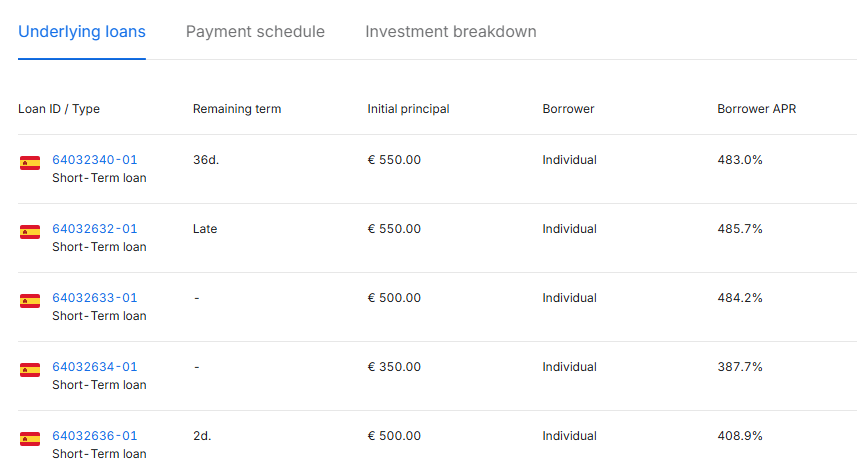

To understand what has changed, you need to recall how Notes work. Or more precisely, a Note package. Issued by an intermediary company, it contains loans for many end customers (NOT one – that’s why it’s called a package). On the other hand, such a set of Notes is “purchased” by investors on the Mintos platform.

To illustrate, here is an example of one package of Notes – 5 loans:

Going further, what happens if there is a delay in one borrower? First of all, it does not affect the other borrowers who are repaying the installments. On the other hand, investors who participate in a given package of Notes receive information about the delay of part of the package, adequate to the amount (e.g. 15%).

This means that the delay cannot be calculated by viewing the active loan statements in the panel, because in most cases the delay is only partial.

On the other hand, Mintos calculates delays on its own on the portfolio tab. I decided to verify their mechanism of action.

I calculated the delayed arrears in Notes once, taking into account the proportionally delayed parts of each Note. It turns out that the Mintos platform correctly shows the delays of Notes in the portfolio summary section (it deducts the already paid installments). The discrepancies are around 3%, I assume that they may be due to the system calculating the delays overnight.

To conclude this long paragraph, I have decided to change the way in which I calculate delinquent loans for Mintos based on:

Delay = Summary of delays presented by Mintos + Pending Payments + Overdue.

To clarify the remaining items:

- Pending payments are payments reported by the intermediary company as already paid. However, Mintos still has not seen this money.

- Overdue payments in which intermediary companies, despite repayment problems, did not fulfill the redemption procedure. Here Mintos fights the hardest and describes each case separately on the platform (see Kviku with rubles).

While writing a paragraph explaining the behavior of Not packages, I wonder if I should put these definitions in the next Mintos review update, what do you think?

—

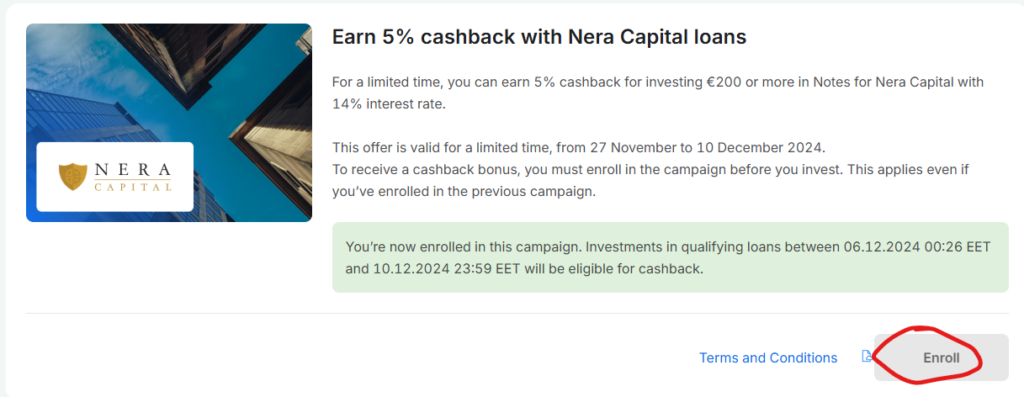

Apart from analysing delays, I was tempted by the campaigns of the intermediary company Nera Capital and deposited an additional €6,000. The promotion is valid until December 10, so you can still take advantage . It is important to invest only in Nera loans with 14% interest (no more, no less), a minimum of €200 and apply for the programme in the campaign tab!

If you want to start your adventure with Mintos platform, please check out my review: Mintos Review (2024): 14.89% return after 3+ years

Signing up using my invitation link, you will receive €50 for investing €1,000+ and a 1% bonus on the amount invested within the first 90 days.

Mintos (Rubel rosyjski ₽)*

As a reminder, since the war in Ukraine, the position is in the process of being paid out . Currently, the last company to be paid out is Kviku.

In November, Mintos sent a reminder that it was negotiating a new agreement for the sale of arrears with a third party. The previous one (from December 2023) did not bring any results.

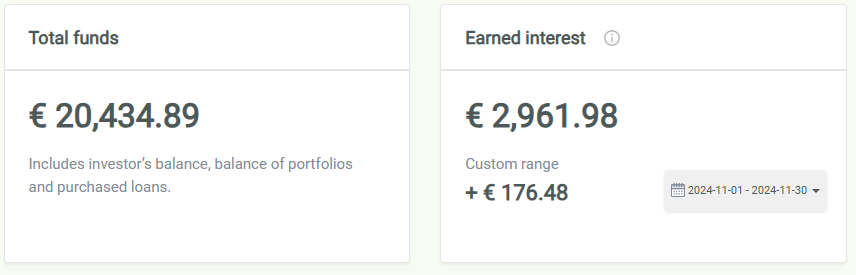

Robocash*

After a recent major topup (amount exceeding previous portfolio size), position remains stable with no defaults . Interest rates are back to a pleasant 10%+.

Unfortunately, the platform is increasingly experiencing cash drag awaiting for new loans. At the beginning of December, it was 1,000 euros. Compared to the size of the entire position, it’s not much, but it’s worth watching.

If you don’t know how to start your adventure with Robocash. Feel free to check review and detailed description of my strategy: Robocash Review (2024): 12.65% return after 2 years

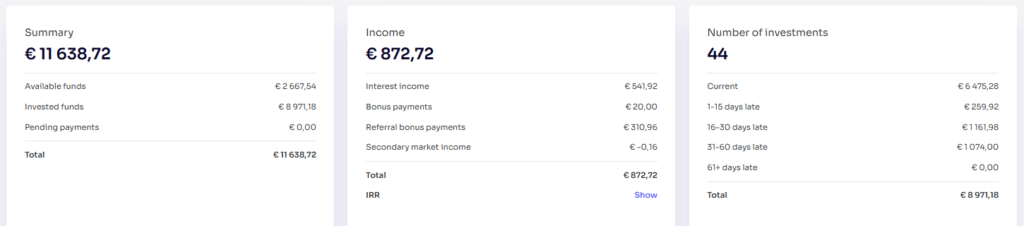

Esketit*

Stable returns returned to the assumed path of 11%+ . As in the case of Robocash, cash standstills are also visible here in anticipation of new loans. Unfortunately, the scale is much larger, reaching over 20% of the account value.

By registering using my invitation link, you will receive a 1% bonus on the amount invested within the first 30 days.

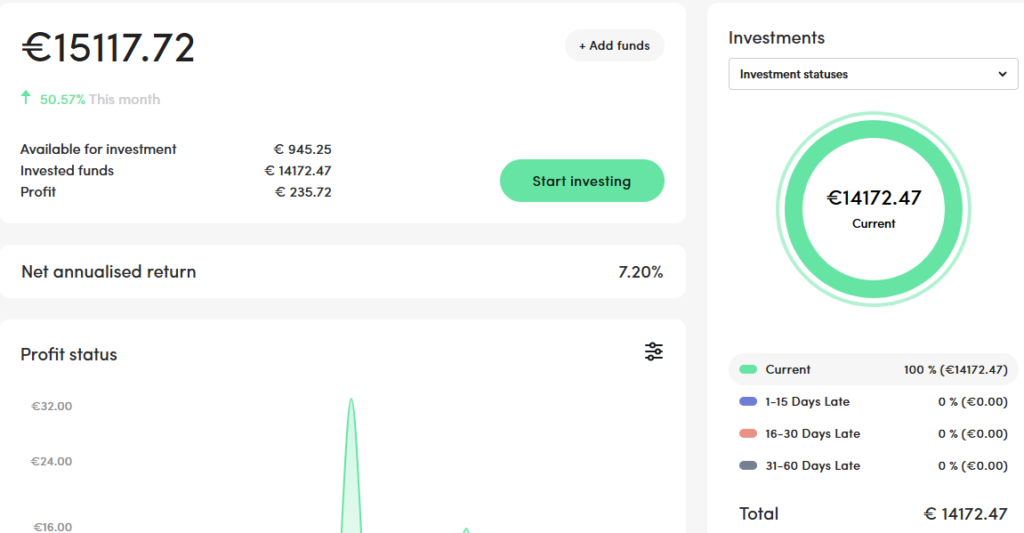

PeerBerry*

I managed to partially solve the problem of supply of new loans. Despite the set automatic investment strategy, you can hit moments (especially in the morning) when positions are “thrown” onto the platform and available for manual intest. In this way, I managed to fill the portfolio with new positions. Interestingly, in this way you can even find positions with an interest rate of 10.5%.

It’s not ideal and requires patience, but it helps to temporarily cope with the downtime. If this situation continues, I might just write a machine to do it for me in the morning.

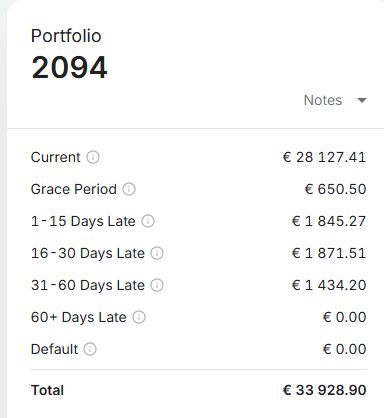

Solving the above problem and adding the argument that this is the only platform that does not have any delayed loan with a €15k investment. I made a decision to invest another tranche of +€5,000. I am still wondering if the €25k barrier, which gives +0.25% bonus to return, is worth getting.

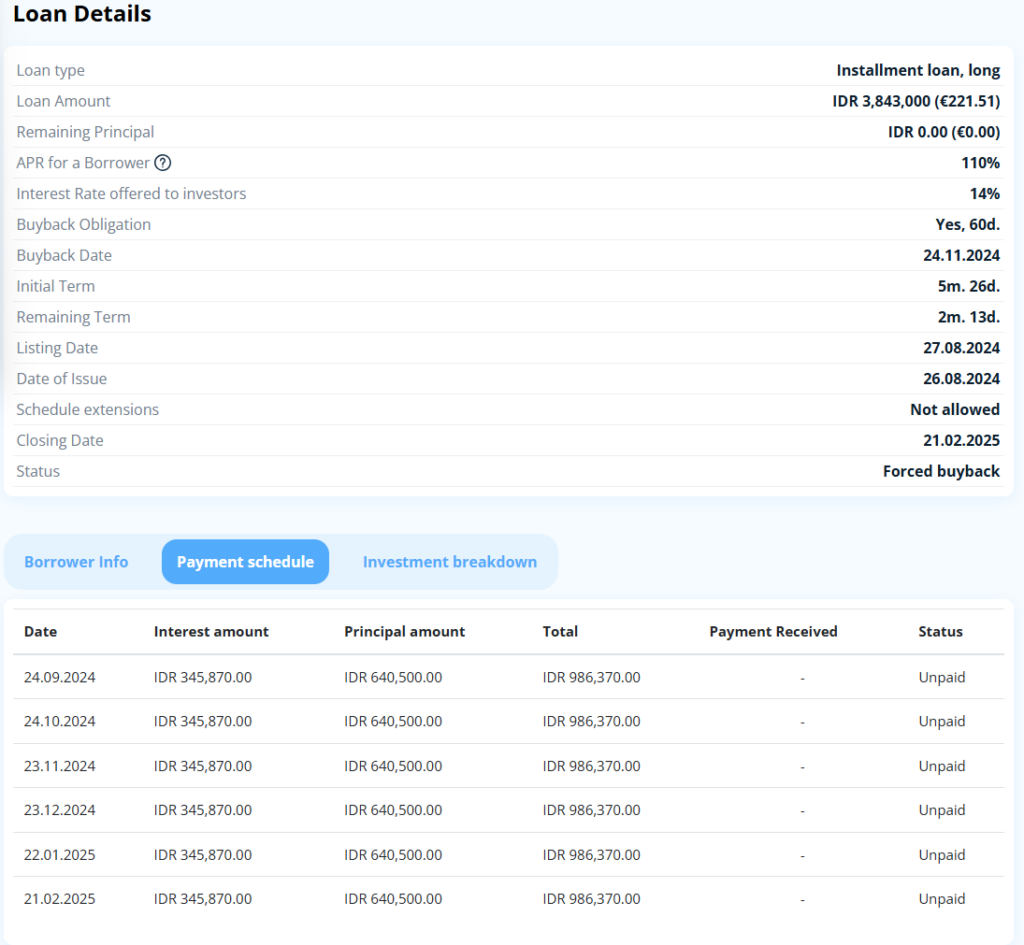

Income*

Less than half a year of positions in the portfolio and I have already experienced the mechanism of buyback loans on the platform. Other platforms have failed to do this for 4 years 😅

This allowed me to check the mechanism of its operation and, more importantly, the interest rate on loans bought back in this way. Let’s take one of the loans bought back with buyback for calculation:

€221.51 total loan amount, with an interest rate of 14% for the investor. Of which my share is €11.12, I should receive €0.1297 interest per month, or for ease of calculation €0.00426 per day.

The delay in repayment occurred with the first installment (after 28 days). After another 60 days, the buyback process was initiated. So in total after 88 days:

- With a standard instalment payment, I should receive €0.3753 in interest.

- Thanks to the buyback procedure through the intermediary company, I received a refund of €11.12 of capital and 0.38 of interest.

To sum up, the intermediary company covered not only the capital, but exactly as much interest as results from the entire life cycle of the loan (including the delay).

—

I admit that I expected this type of disruption on a platform where loans with an interest rate of 14% are common. However, I am glad that despite such large delays, returns remain at 12%+, which means that there is a constant rotation of old delays (paid with interest) to new ones. So there is a circulation of invested money, and that is the most important thing 😜

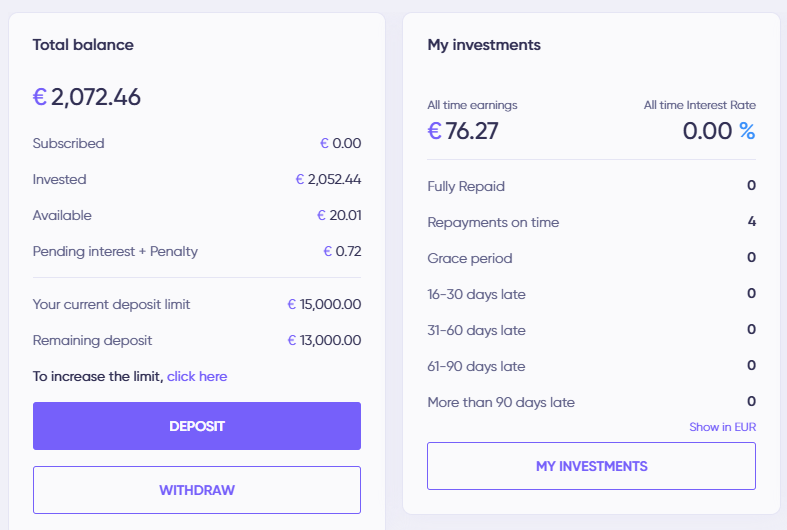

Debitum*

As announced, I am adding another block to my portfolio. Unlike the last one (Income), Debitum is a regulated platform with a lower level of risk . Of course, I do not take anything for granted. Only time and possible problems with repayments will verify the reality of the slogans proclaimed on the platform.

Model The Debitum model is similar to many other platforms. It connects intermediary companies with the investor. Why did I choose Debitum?

- Regulated brokerage firm (license no. 06.06.08.728/537 ).

- Increasing the portfolio with regulated items. Debitum requires intermediary companies to secure loans with various assets (e.g. collateral for assets at 90% of the loan value)

- They can boast of unpaid loans at 0% (it is worth considering that they are a relatively young company)

- Still high interest rates (from 12% to even 16.5%) + cashback promotions

The downside is definitely the poor auto-investment system, for now the best way to “catch” good positions is manual investment. It’s too early for a review, for now let’s look at the results.

My investment started in September, I have not noticed any delays so far, the interest rate itself is at 13%.

ETF

ETF position still on an upward trend. No major changes here, no plans to increase this position.

(*) I play open cards. Links marked with an asterisk are affiliate links. If you use them, I will receive a commission. It won’t cost you anything, and often you will get a bonus too – More information can be found on the pages under the specific links.

(**) Due to the nature of the stock market, income should be understood as potential until the position is realized.